I’m a big fan of frameworks, they help us categorize and make sense of the world around us. As you are building products, frameworks help you systematically approach the process. I’ve always been intrigued by Reid Hoffman’s quote that mapped consumer social products to the seven sins. This was a great framework to map a product strategy to a core human instinct, in this case, vices.

With the consumerization of enterprise software can we do something similar? can we get derive a systematic framework that represents emotion in the enterprise world?

Frameworks are best explained through examples, let’s take a specific example of software products designed for Investment Managers. A little bit of context before we begin. The world of people who invest (investors) can be broadly divided into two areas

- Retail: This is you and me, mom and pop investors. Our most common use case is to directly purchase investment products, we buy stocks, bonds directly from brokerages like Etrade. We have products such as checking accounts, credit cards and life insurance from banks. You, the consumer is directly making the investment decision. For products addressing this user segment, the relationship resembles a business to consumer (b2c) relationship.

- Institutional: These are the big guys. Think of them as specialized Investment Professionals that manage other people’s money (OPM). Venture funds, Investment Banks, Private Equity and Pension funds are examples of Institutional investors. A typical Institutional investor business has a General Partner (GP) and multiple Limited Partners (LPs). The capital to invest comes from the LP’s and the GP is making investment decisions on where to invest the money. Hence the term other people’s money. For products addressing this user segment, the relationship resembles a business to business (b2b) relationship.

What are the key emotions that are applicable in this context? What are the key drivers and emotions for the constituents?

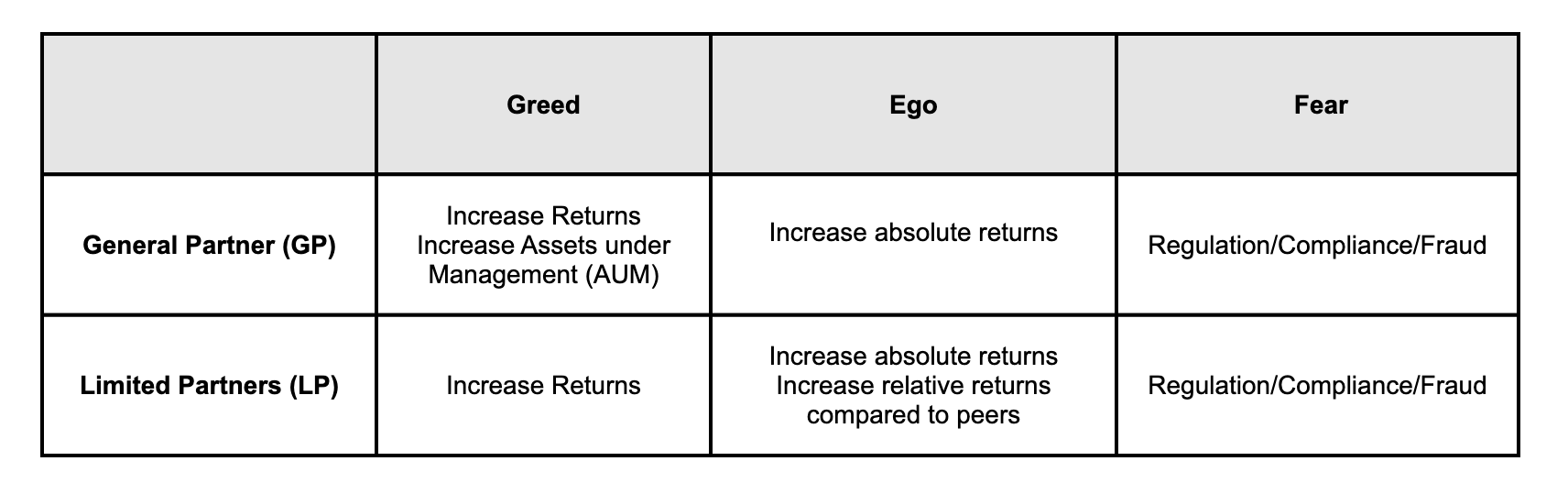

For a general partner, the compensation model is usually and 2 and 20 i.e a 2% management fee and 20% of the profits (carry). This model aligns the incentives between the GP and the LP’s – the more money we make together, the more we get richer together. Mapping this to emotion, this is greed – greed for GP’s is increasing assets under management and getting returns that get them that 20% carry.

Investment returns are how GP’s are compared with each other. Picking good investments (generating alpha) requires skill, the more you beat the benchmark, the more you can claim skill, the more your ego gets a boost! i.e investment returns map to the ego. If you have better returns then you will also have more assets under management as more investors will flock to you. So for GP’s better returns and big AUM = bigger ego.

Finally, investment management is a regulated business. If you mess up in the compliance, fraud area the government will come after you. You will be shut down, it is good to be complaint and fearful of the consequences. This is fear.

Let’s look at these same emotions from an LP’s perspective. LP’s are compensated via investment returns – that is the primary reason that they are investing. So greed for LP’s is about getting great investment returns. Similar to GP’s, LP’s like to compare themselves with other LP’s – did they choose better funds than other LP’s? i.e did they get better relative returns than other LPs? Ego for LPs is getting better returns than their peers, which is indicated by – did they pick the right funds to invest in? Did they back the right GP? The regulatory aspect is the same for LP’s just like it is for GP’s, they have to be compliance with all regulation – the fear factor is the same across both LP’s and GP’s. Labeling and mapping the core emotions to the underlying business model gives us our framework.

Ok, that’s all great, you have a framework but how does this help me? Two examples

If you are building a product for this space, what is the feature set you want to target first? The greed/fear axis is an interesting tradeoff. Most established customers have more to lose by messing up regulatory compliance (fear) than by enhancing returns (greed) – so if you want to sell into incumbents, a fear-based feature set is probably a good initial bet.

If you are prioritizing features for a current product, who is the end customer and what do they care about today? Add Greed/Ego/Fear as another variable against your features that you are prioritizing. If you are selling into venture funds, as this is a lightly regulated business maybe fear-based features should just be off the table or should be MVP level only. As an example for the VC customer set between the two features, one – a feature that helps to automate the closing process with LPs vs two – a feature that provides enhanced compliance reporting to LPs – pick feature one as this appeals to the greed aspect of GP’s. Your customers will be more inclined to pay for this feature.

What do you think? Are emotions a useful approach to consider?