Part two of the deep dive into the Buy now pay later (BNPL) market. In part one we dug deeper into the core product and its history. In this post, I dig deeper into the value proposition of the product.

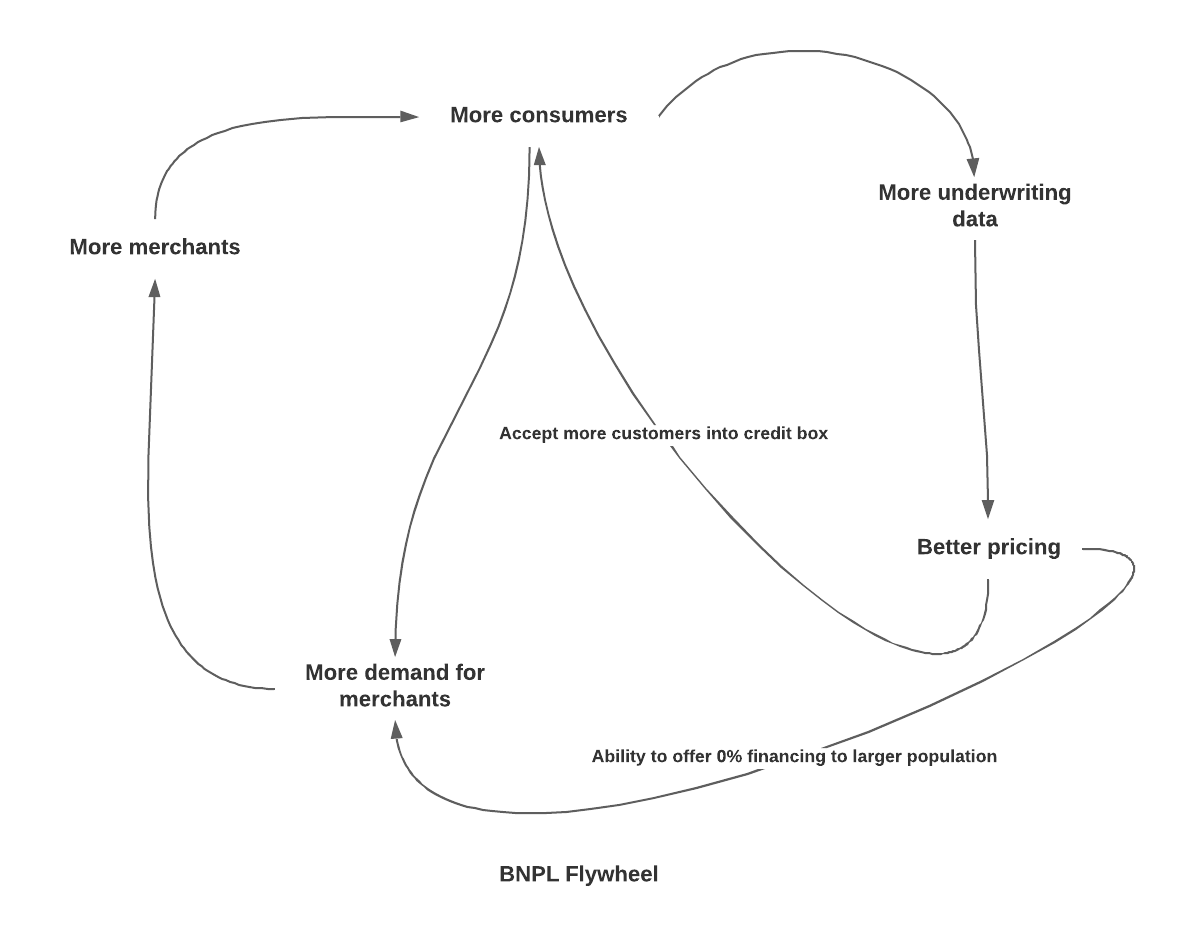

A common misconception about this market is that it exists only to serve only the needs of the consumer. It exists only to make consumption easy. This is wrong. This a two-sided platform product. This product exists to help both sides of the transaction – merchants, who sell items and the consumers who purchase them. The fundamental axiom in use here is that extending credit greases consumption. Consumption for consumers is revenue for merchants. By offering various credit constructs and financing options to your customers you are enabling them to buy more of your products. This increases your revenues as a merchant. There is immense value in this product as a conversion tool.

Consumer retail is the largest sector of the US economy, it’s a ~$5T market, a large market by itself. Also, the internet and more recently Covid 19 has accelerated the move of this market into eCommerce. The BNPL businesses are internet-native and as a consequence, they can get their growth flywheel going quicker than a normal offline credit business.

How is the product structured for the consumer?

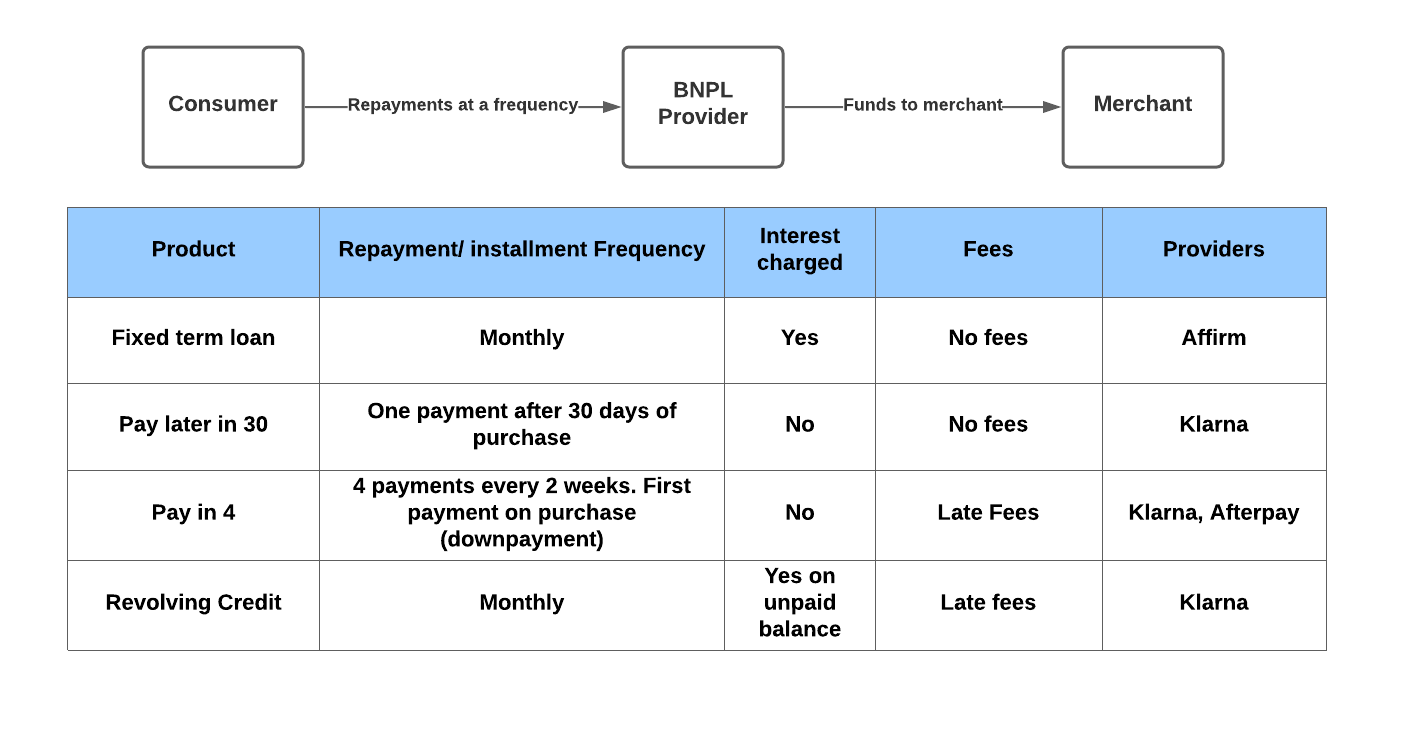

In this post, I am restricting myself to the three main players in the US Klarna, Affirm, and Afterpay. In a subsequent post about competitive dynamics, I will dig deeper into the new players (Shopify, PayPal, et al). The core concept of these products is to extend financing and each company is accomplishing that in a few ways.

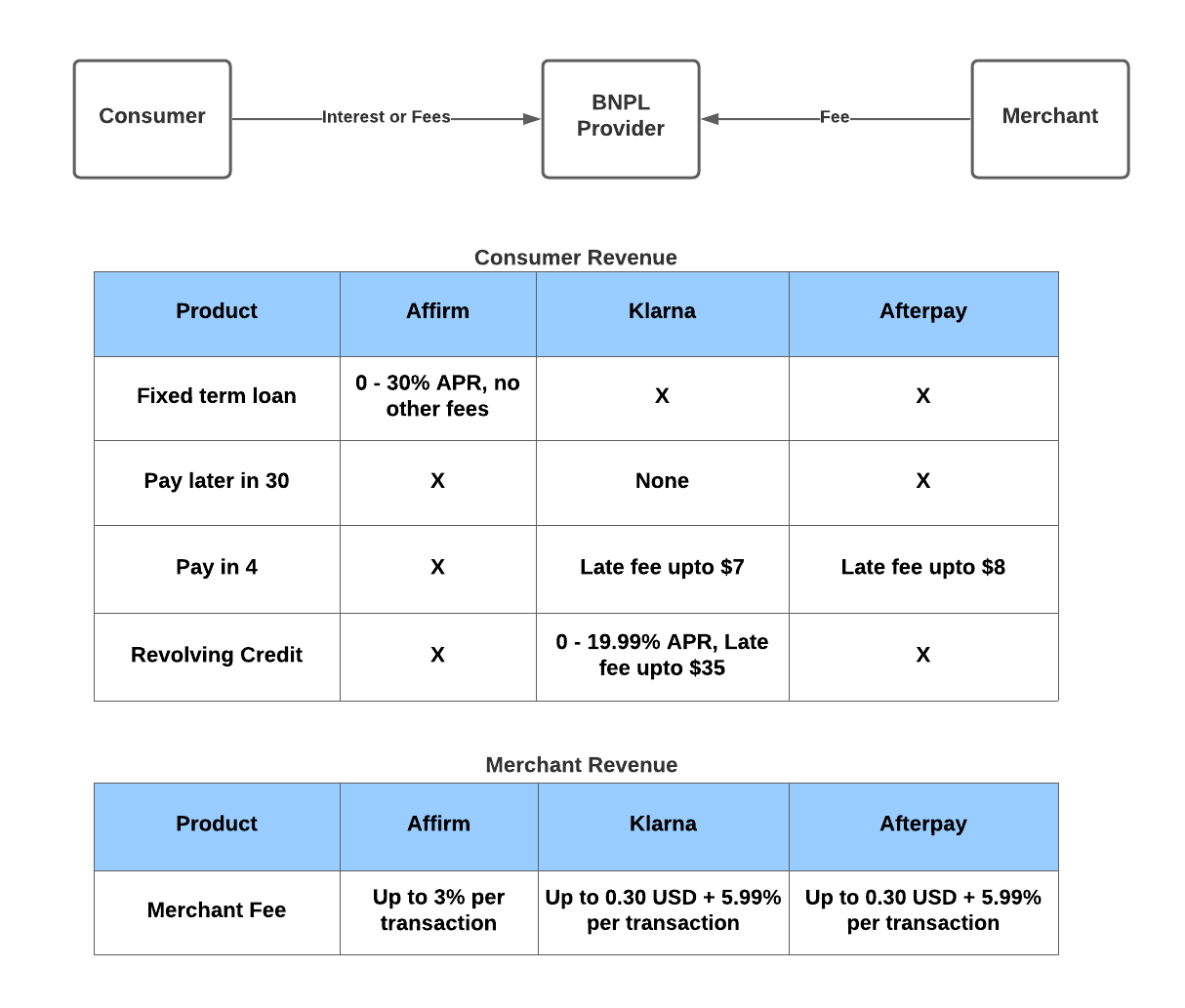

Affirm is the simplest to understand. It is a point of sale fixed-term loan. Exactly like any other consumer loan product, you borrow a fixed amount of money (the purchase price of the good that you are purchasing) and make fixed monthly installments of payments plus interest for the term of the loan. Affirm is unique in that it does not any additional fees to the consumer. Most loans always have some sort of origination fee and/or late fees – affirm charges none of that. The only cost to the consumer is the interest portion of the monthly repayment.

Klarna offers three products and is somewhat of a pioneer in the space. The easiest product to understand is the Klarna financing product. It is exactly like a credit card. If approved, you get to spend up to a credit limit. You can pay off the balance in full every month or revolve the balance and pay interest on the amount you revolve. Exactly like a credit card, except for the fact that you can only use this product at merchants where Klarna is accepted. It is not a general-purpose credit card that can be used anywhere.

Klarna also offers a pay later in 30 days option. With this option, you can effectively defer paying for the purchase for 30 days. This is effectively a 0% interest loan for 30 days. If you do not ever make the payment, you are cut off from Klarna and cannot use the service again. Klarna does report delinquencies to the credit bureaus. There are no fees or interest in this service.

The final product in Klarna’s suite is the Pay in 4 product. This is truly a different product than what existed in the market. As the name indicates the purchase price can be split into 4 payments at no interest. The time between the repayments is fixed to 14 days. The first payment is charged at the time of purchase. So for a consumer to use this product, they need to have an existing credit or debit card and have enough funds for the first payment to go through. If the automatic repayment every 14 days fails for any reason you are charged a 7$ fee. If you do go into default Klarna does report delinquencies to the credit bureaus.

Afterpay’s product offering is the same as Klarna’s Pay in 4 product. That is the only product they offer.

What consumer need does it fulfill? Who does it appeal to?

All these players intend to provide an easier way for consumers to buy things. By providing a loan (in the case of affirm) to the pay in X time without interest options, BNPL providers are reducing friction in the buying process. If the primary consumer hurdle to buying your product is the sticker price, BNPL helps you overcome that hurdle.

Klarna highlights an interesting use case for the Pay in 30 product – avoiding the payment issues with returns. The pitch is that if you want to try something and return it, use the pay later in 30 product as a way to only pay for the items at purchase. If you return some items within 30 days, your Klarna payment will automatically adjust down to only pay for the items you keep.

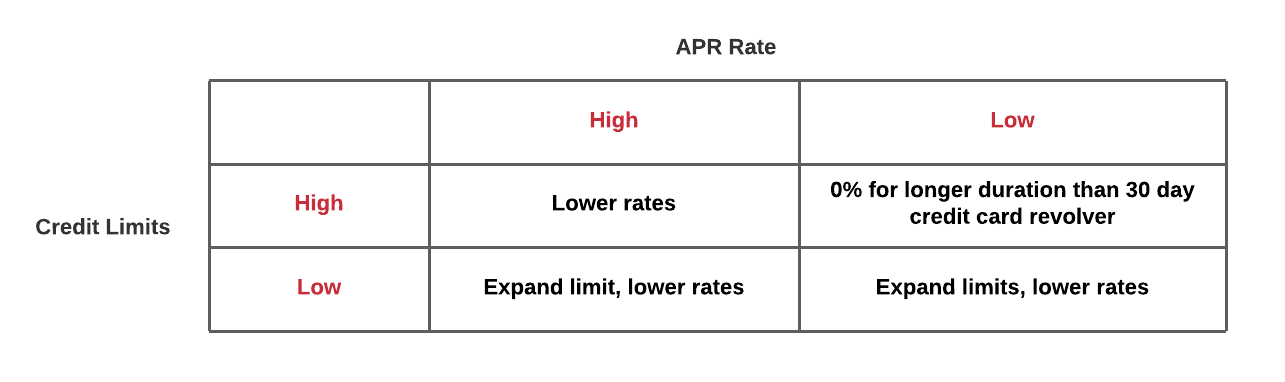

For customers with credit cards and low credit limits, this may be an interesting option, but I’m not sure of the customer value this payment plan provides. For customers paying with debit cards (i.e cash), this product is super valuable. Using this product you can conserve your cash flow and only pay for things you keep after 30 days. The following matrix highlights the use cases for customers with available credit (Credit cards).

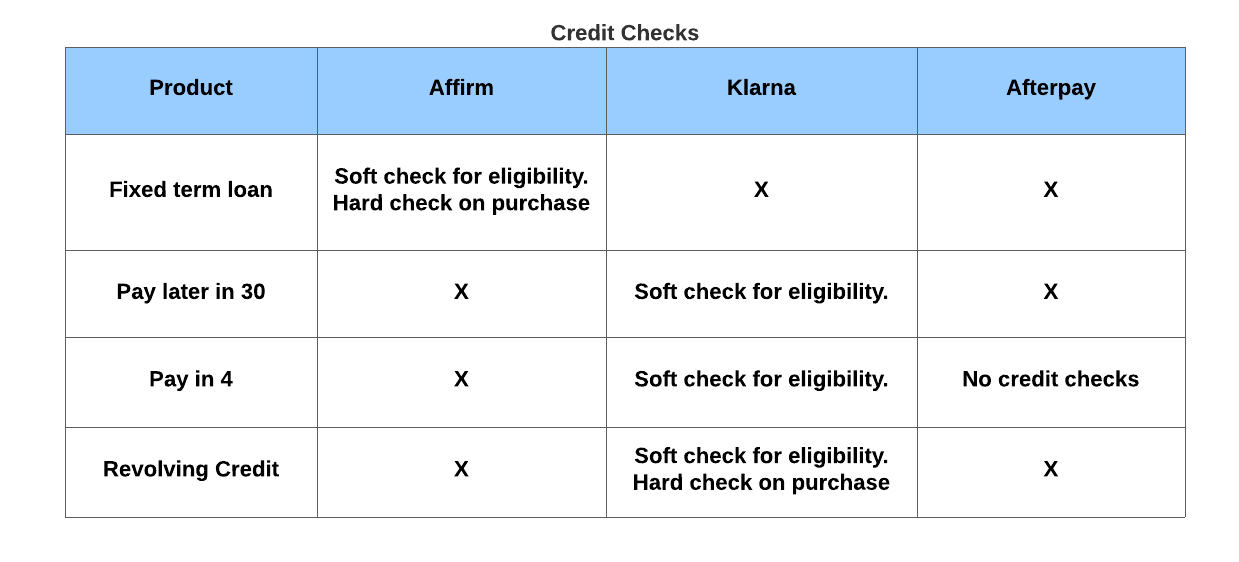

For consumers who cannot qualify for credit cards or who only use cash/debit cards, these options are a godsend. You have access to financing options that you were shut out of. Another huge factor is the rational fear of how these products affect your credit score. In the US, your credit score is pretty much everything. This single score determines your place in the financial services hierarchy. Great scores equal more options and lower scores equal a lifetime of no access and high prices and fees. Each of the providers handle credit checks differently (see table below).

How is this useful for merchants?

The merchant pitch is pretty simple. Offering financing options increases sales, period. Why go through the hassle of setting up your financing program? Just use us, we integrate well with existing shopping management e-commerce providers and we also have easy to use API for custom integrations. We will assume all the customer fraud liability and you get paid the full purchase price of the good (minus fees) within a few days of the purchase transaction. We also give you slick marketing tools that you can use to promote BNPL to your customer base to increase attach that increases your units sold.

The BNPL players also provide the opportunity to generate more net-new demand for the merchant. Let’s take affirm as an example. Once a customer has signed on to use affirm, it now has a relationship with that customer. All the payment management happens via a mobile app that customers now have downloaded onto their phone. As the number of customers of affirm increase, more users start using its app and are now a captive audience, an engaged audience. Affirm is in effect aggregating customer demand and can now push other products from the same retailer or other retailers to that audience. It is the ultimate cross-sell. Affirm now has become a shopping destination via which its customers discover new products. Now retailers have access to this customer demand to sell through – i.e it’s an avenue to get more customers. This is very valuable to merchants.

So who is paying for this?

Somebody has to pay for this :). The primary revenue source is merchant fees with some revenue coming in from interest payments on the revolving credit products. A summary table below

The merchant pricing here is super interesting. Average rates for credit card acceptance run about 1-3%, so compared to credit card these fees seem pretty high. But merchants must be seeing value as this product enlarges the customer set that can purchase their products. So all of the revenue is incremental.

An aside into 0% financing

I am super curious about this direction of offering 0% loans for a longer duration on a revolving credit basis. Affirm is well know for this especially with Peleton. With large ticket items, there is a natural fit for 0% financing. It is a no brainer if you can afford the purchase price to just go ahead and still pay over some time at 0% and exploit that time value of money. I suspect that a large portion of Pelaton’s growth is due to the 0% financing option. This is a clever strategy from Affirm. For low risk (high credit score) customers, which tend to be affluent households, this is a great way to take market share away from credit card providing banks. These affluent consumers can probably buy that Peleton on a credit card and pay the entire balance off in full every month. But by offering 0% financing, affirm takes them away from their credit card and – thus eroding the bank’s margin from fees that they charge merchants. The merchant fee now goes to affirm and not the credit card ecosystem. In cases where the consumer repays affirm via ACH or debit, it further erodes the credit card network margin as the entire transaction now went off-network. The credit card network got reduced revenue (as debit interchange % is less than credit card interchange) from this entire transaction!

Strategically, this pattern is the classic internet-compresses-margins pattern. As businesses transact more online there will be internet native players who can build natively on the internet for better, faster, and cheaper. The margins on the revolving credit industry are getting compressed!

In the next post, let’s dig deeper into the publicly available financial statements and information. Let’s explore the viability of these businesses!

Look forward to part 3 – curious about their defensibility with so many players entering this market. Who are the winners and losers?