In the last post, we explored what drives an economy (spending) and the levers that a government can use to restart the economy after a crisis (monetary and fiscal). Since 2008 monetary policy has paid the dominant role, but in 2020 fiscal policy is finally making a comeback. Fiscal policy has a direct impact on consumers’ lives as the main objective is to get cash into consumers’ hands so that spending continues unabated.

How to get cash to citizens?

It is logistically impossible for a government entity to show up at every citizen’s doorstep with a truckload of physical cash. Besides the obvious problem of logistics, there are also problems with confirming identities and physical record-keeping. Especially when governments are handing out money, they want to be very particular that only their citizens are getting the cash and there are no cases of freeloading (via fraud, etc). Direct transfers are a politically charged issue – there are always allegations of a slippery slope, nanny state, and communism that get thrown around! You have to get this part right.

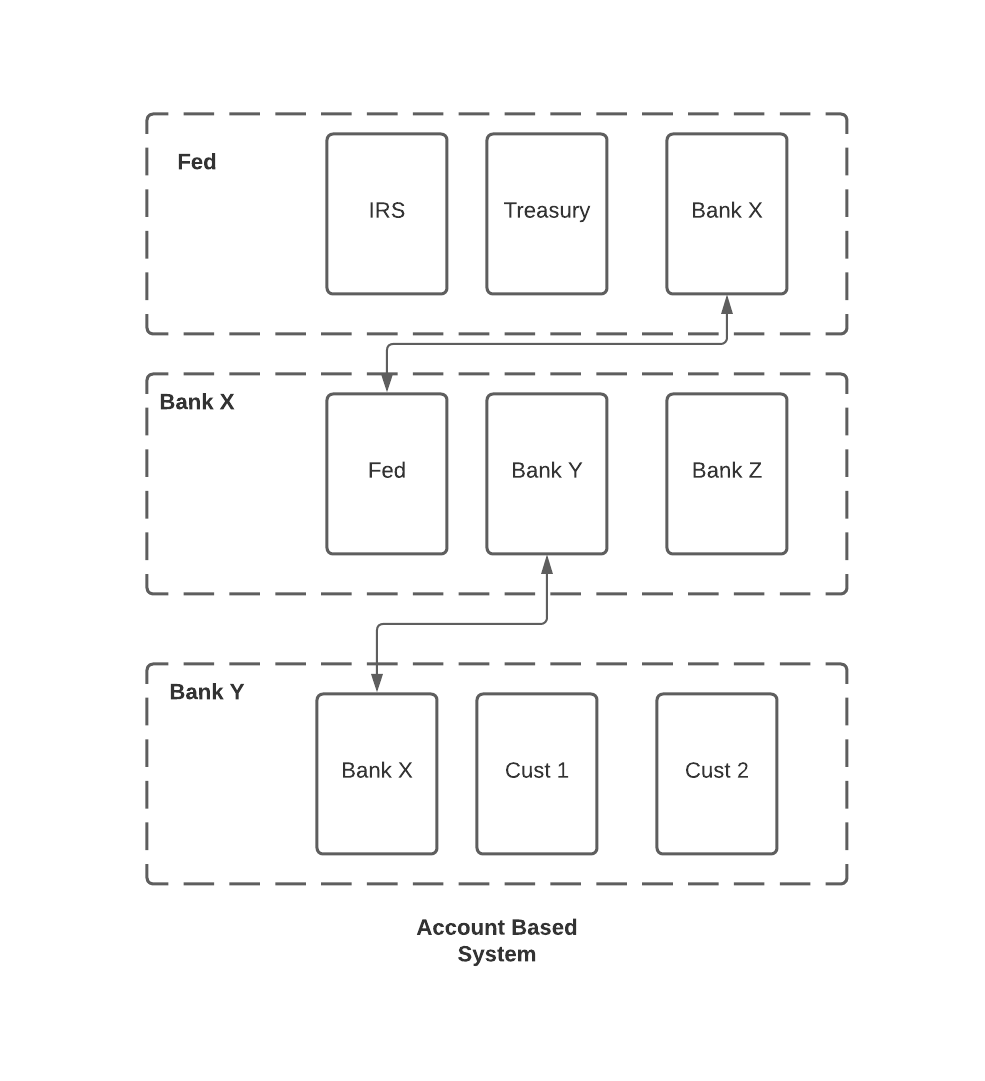

The next best way to get cash to citizens is via an intermediary i.e the banking system. The modern banking system is an account-based system. The core abstraction for any monetary system is the ledger, it’s the record of transactions i.e who owes how much. In the banking system, “money” is really an entry in a ledger somewhere. You can think of the entire system as a series of cascading ledgers. Each account is really just a ledger that contains details of the transactions at that level of the tree. The fed is the master ledger of the government and has the banks and various parts of government as its sub-ledgers. Each bank has other banks and their customers as their sub-ledgers. Every customer account/ledger at the edge of the system can be traced back to a central account at the main bank (fed) via its intermediary banks. This system is known as correspondent banking which is an account-based system. In the US account-based system the routing number + account number combination is used to identify the end customer account. The account number is the index to your ledger transactions at your bank and the bank is identified by its routing number. You can think of the bank routing number as its account number at the fed which is the master bank.

In the US the only organization that has a lot of consumer routing and account information is the IRS. There are only two things in life that are certain, death and taxes :). In the yearly ritual of filing your taxes as a consumer, you fork over your bank details to the IRS in order to pay your taxes or get a refund. Thus the IRS was the government organization that sent the stimulus funds to the end consumer. The transaction flowed through the banking system as follows

- The Fed is the master bank and has an account for the IRS and Treasury

- The Treasury account is deducted and the IRS account is incremented (IRS has money).

- The Banks ledger at the FED is incremented, the IRS ledger at the fed is deducted for the amount to be transferred (the money has effectively moved over to the bank)

- The Bank then at its end increments the individual’s account ledger in its systems. This reflects your increase in your account balance.

- You have the cash to spend.

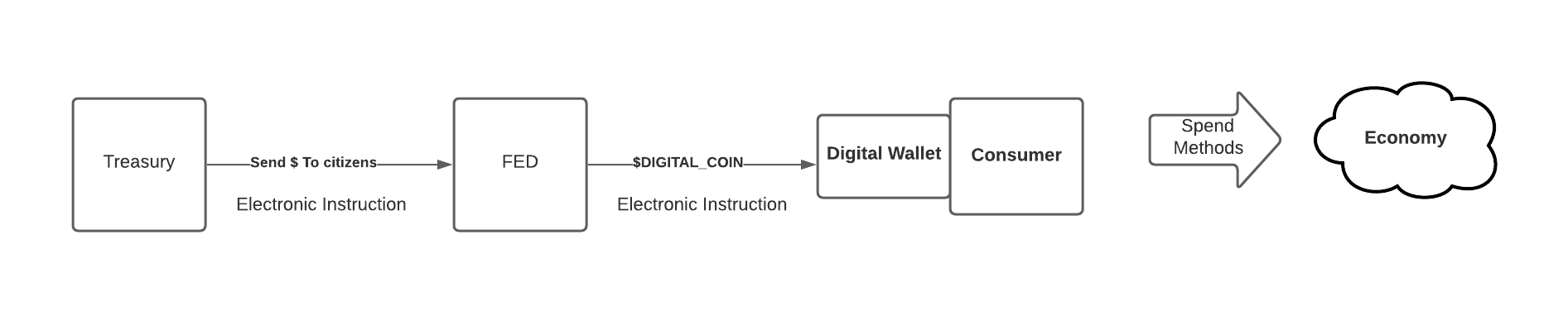

This process in a roundabout way gets cash into the hands of the consumer. This process is completely digital, but it is still intermediated by a system that was built to handle physical cash.

So what has this to do with CBDC’s?

Wouldn’t it be great if there is a direct digital representation of physical cash that bypasses this entire intermediation process? I believe CBDC’s are this magical thing. CBDC’s are exactly like physical cash but can directly be loaded by the government into the consumer’s digital wallet. You can entirely skip the intermediated banking system and go direct to the consumer. It’s the internet version of distribution that we are familiar with applied to governments. DTC all the way!

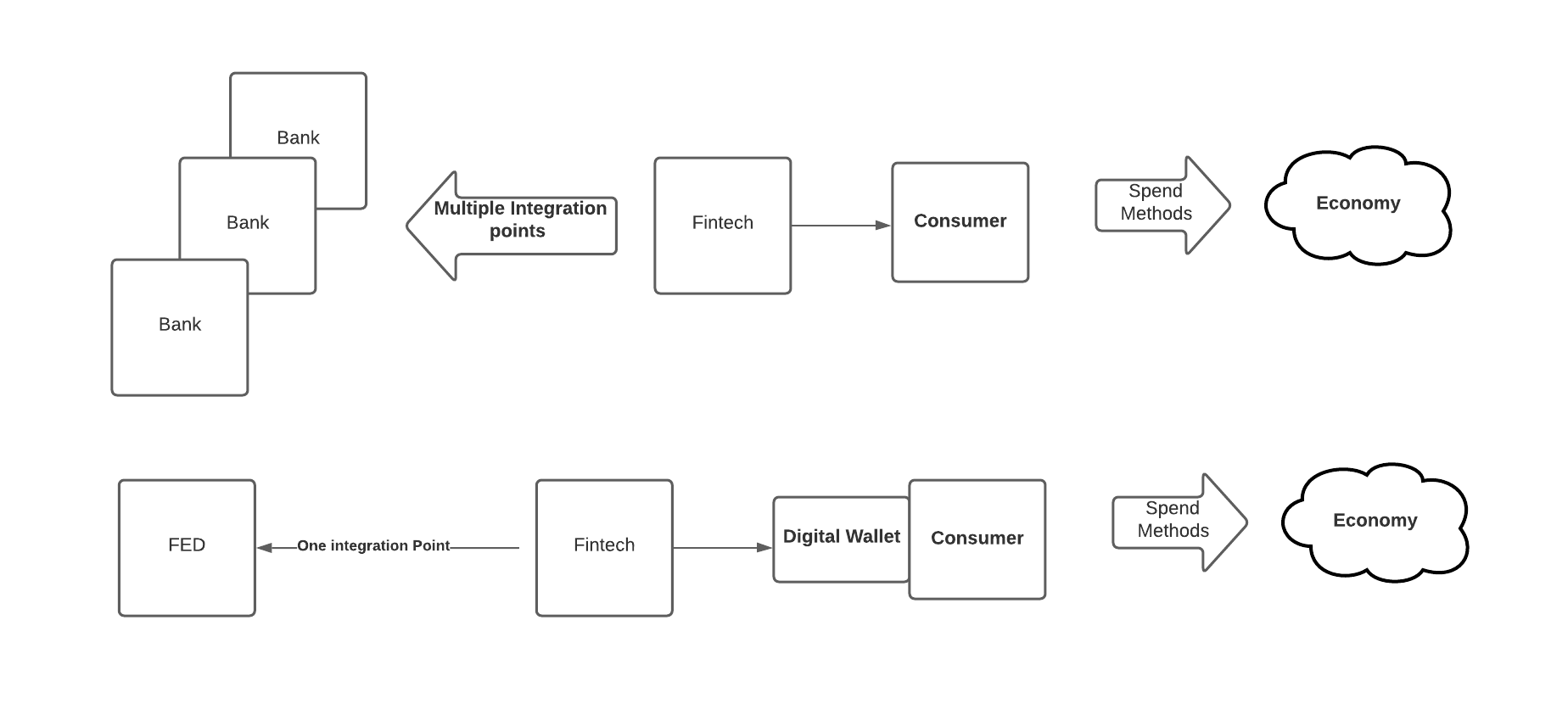

Why does this change everything for fintech?

All the fintech providers spend a good chunk of their time and resources integrating with the banking infrastructure because of the account-based nature of the intermediation. If you view the consumer’s financial life as a system, the most important part of this system is the input – i.e where does the consumer’s income/money enter the system? Due to the current account-based structure, a consumer could have accounts at any of the multiple banks that exist in the US. To get a handle on all the inputs to your fintech product offering you have to integrate with all the banks – and there are a lot of banks!

Enter CBDC’s. If they take off and it is all direct to consumer via rails provided by the government, the complex intermediation is gone, poof. There is only one interface that matters – the interface to the fed.

One simple point to point interface to rule them all. That changes everything…

One Comment